If you’re running a company — a real one or a startup — you’ll want to remember the story of Fred Futile, CEO of Stagnant, Inc.

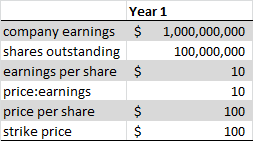

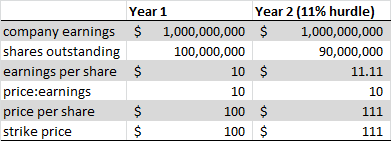

The compensation committee of Stagnant, Inc. saw fit to award Fred stock options equal to 1% of the shares then outstanding. This was intended to give Fred an owner-like interest in the business and incentivize him to increase the value of the company. Stagnant was at the time earning $1 billion each year on $10 billion of equity. There were 100 million shares outstanding, so earnings per share were $10. The company traded at a price to earnings of 10, so the option price was set at fair market value, $100 per share. Here’s a table summarizing the vital statistics:

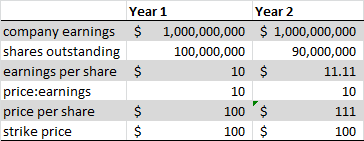

Now Fred did an ingenious thing. Rather than work hard to change Stagnant into something more than the marginally billion-dollar business that it was, he used the year’s earnings to repurchase shares. Look what happened:

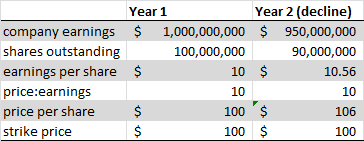

The one billion dollars of earnings bought ten million shares at $100/share. Assume the company traded constantly at a P/E of 10 and you can see the trick: just by withholding money from shareholders, Fred was able to put his options in the money and make himself $11 million. He didn’t have to improve the business at all. And if that doesn’t surprise you, look at this: if in Year 2, instead of holding constant, earnings had actually declined by 5% due to Fred’s negligent management, Fred would still have been in the money on his options:

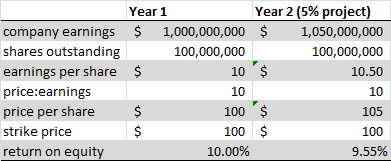

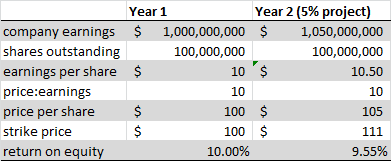

Fred was gaming the system then, to be sure, so let’s look at what would have happened if he had tried to reinvest the earnings into some seemingly worthwhile project that earned 5%. We’ll add one row at the bottom for “return on equity”. We started with $10 billion in equity, and then Fred will reinvest $1 billion at 5%.

Do you see how the return on equity decreased? Fred’s seemingly worthwhile project gave his investors a worse return on investment than if he had done nothing at all. And oh, Fred is still making millions on his option plan.

The lesson here is that Fred’s option plan is flawed. It’s okay to want to incentivize Fred with options, because as CEO he does have an impact on the overall success of the business. But his options should have a cost of capital or time factor. This way, it’s clear to Fred that if he can’t use company earnings to match the current return on equity, he should pay the money out to shareholders. Take a look at this new and improved option plan where Fred’s strike price increases at 11% each year:

Now if he tries his repurchase scheme, he doesn’t get rewarded (at least, not as much; I left off some pennies and he’s still technically in the money here).

The same is true (even more true) if he tries his unsuccessful project:

Option plans with hurdle rates should be used for every CEO or other executive that insists on option plans. This much better aligns his or her incentives with those of the investors, and comes as close as you can get to having them just buy in to a large amount of stock, which would be best of all.

The inspiration for this article, including Fred Futile and Stagnant, Inc., is owed to Warren Buffett and his annual Letter to Shareholders, 2005 (click here to read and search for “Futile”).